You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Kev3188

Veteran

An interesting read. When I read it yesterday, this part really jumped out:

"You might be surprised to know that with its joint venture partner JAL, American has onlyone two fewer flights per day as compared to Delta between the Continental US and Asia."

Definitely surprising...

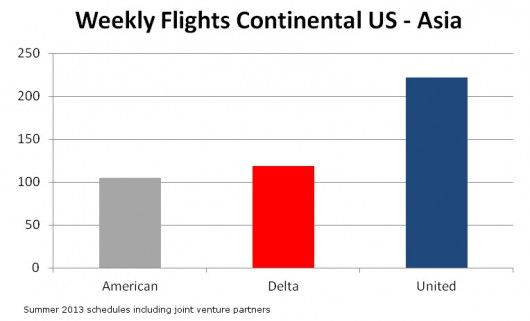

"You might be surprised to know that with its joint venture partner JAL, American has only

Definitely surprising...

WorldTraveler

Corn Field

- Dec 5, 2003

- 21,709

- 10,721

It didn’t really take reading too far into the article you cited, E, to realize that either the author is truly clueless about how the US-Asia market works or else is so biased that they think if they throw up a bunch of biased statistics, no one will notice.

And, yes, this is a long post because it contains real data and analysis. Those who can't absorb or discuss this kind of data should just move along.

Copying and pasting a few poorly written articles doesn't begin to provide any understanding of the subject.

Let’s start w/ the author's assumptions, which form the entire basis of what is wrong w/ the analysis.

“First, I’ve left off the substantial Delta and United operations that go from Tokyo to secondary cities in Asia. That would make Delta way bigger than American, but I don’t think it matters. American can get that benefit through its joint venture partner JAL. (United also gets that through ANA besides its own Tokyo hub.)”

Say what? You want to exclude DL’s ability to offer connections within Asia but you acknowledge that JL and ANA do the same thing for their Asian partners? So you want to just include TPAC flying as if that someone is all of the market. Sorry, but the logic is seriously flawed.

But let’s look at just the US-Japan market since AA plus JL should help provide mass to help compete with DL and UA plus NH.

We can look at two data sources: DOT revenue data which is heavily partitioned between US and foreign carriers; foreign carriers only have to report revenue to the DOT for operations that involve their JV partners. Thus, there are huge portions of the total market that are hidden from view. US carriers, however, report on the exact same basis to the DOT so revenue data for AA, DL, and UA across the Pacific provide the same answers. There is also private industry sourced revenue data from CRS/GDS but it is becoming increasingly unreliable as carriers shift more and more booking activity to their own websites and internal channels, as much as employees and fans of the CRS/GDS data would like to tell you otherwise.

The second data set is schedules data which is not private and pretty self explanatory. While revenue data provides insight into what is actually flown, schedules data is pretty straightforward.

Given the limitations of revenue data noted above, DOT data still unmistakenly shows that DL absolutely dominates the market between the US and Japan among US carriers, carrying 3X more revenue than UA and 11X more revenue than AA. DL carries HALF of all US-Japan revenue in the DOT database. Furthermore, DL’s average fare is 40% higher than UA’s and 75% higher than AA’s. Although JL and NH revenue has to be assumed to not be complete in the database, they do not have average fares as high as DL either.

Now, since the author is trying to figure out how strong carriers are between the US and Asia, the DOT data is also pretty accurate for US carriers. Even if you look at all of the US to all of E. Asia on US carriers on their own metal, DL is within 1% point of UA in terms of market share yet DL carries more revenue on its own metal?

Why?

Because the US-Japan market is still the largest single market between the US and Asia. Almost half of all US-Asia revenue carried by US carriers is to/from Japan. US carriers don’t carry anywhere close to the amount of revenue that is carried between the US and Japan.

But there’s one more piece of really interesting data. Average fares between the US and Japan carried on US carriers are within a fraction of a percent as those to most other destinations in Asia; yet, Japan is a whole lot closer to Asia, which means UA is flying two to three more hours to China and HKG to carry the same revenue that is carried to Japan.

So, revenue data – not just schedules – clearly shows that DL far outperforms AA and UA between the US and Japan both in terms of market share and average fare.

More on alliance partners later.

Second, I’m only looking at flights between the Continental US and Asia nonstop. I’m talking specifically about the Continental US, because both Delta and United have flights between Honolulu and Asia. Those are primarily focused on Asian travelers on holiday so it’s not really relevant to determining how well US carriers serve Asia for their US-based travelers.

So are you really serious about objectively looking at the market or not? It sure doesn’t appear to .

Wanting to exclude Hawaii-Asia flying so that it provides a “balanced look” at the competitive situation is bull.

Last I checked, Hawaii is part of the US.

Also, last time I checked, nearly half of DL’s total flights between the US and E. Asia are to/from Hawaii with a slightly lower percentage of total capacity since DL uses smaller planes on average to Hawaii than between the mainland.

But both schedule and revenue data show that DL carries about half of all revenue between Hawaii and Asia and has higher average fares; DOT data shows that DL's average fares between the Japan and Hawaii are far higher than US to Europe flying even though the distance is about the same.

But the whole basis the author uses to exclude the data is flawed by saying that US-Hawaii traffic is foreign originating. Can he really be serious in thinking that airline companies really care where the revenue comes from? Has it not dawned on him that commercial airplanes generally operate on international flights between two cities in two countries and that the world has a global currency system which allows for earnings in one country to be traded for earnings in another. Does he really think that we should exclude Honda automobiles manufactured in the US from Honda’s global revenues and earnings?

If he does, then he probably should be writing about lemonade stands in Texas where he doesn't have to be concerned about currency issues or foreign earnings.

But you know the real rub in his assumption?

The majority of revenue between the US and Asia originates in Asia, REGARDLESS of whether you include Hawaii or not. So, if he wants to include only revenue that originates in the US, he lops off a good chunk of the market.

But there is an interesting statistic here as well. DL gets a far higher percentage of its revenue, whether you include Hawaii or not, from Asia originating passenger than do AA or UA.

Lastly, I’m including joint venture flights operated by ANA under United and by JAL under American, because since it’s a joint venture, those flights should be considered their own. Sure, there is work to be done before the experience is seamless, but the path is there.

You do realize, sir, that codesharing without a JV is not a charity operation, don’t you? AA doesn’t put passengers on CX metal (since AA doesn’t fly to HKG with its own metal) just because AA and CX are aviation buds. Airlines make money even on codeshares, which his part of why airline labor doesn’t like them. It is not uncommon in the US airline industry for a carrier to keep 15-20% or more of a ticket they sell (not including taxes) even though the passenger does not fly on their airline.

The notion that JVs are the only way that carriers make money working together is completely wrong. AS cannot have a JV with AA or DL because the US does not allow two US domestic carriers to have antitrust immunity and share revenues yet AS makes all kinds of money carrying passengers for AA and DL, and AA and DL make money carrying passengers for AA.

The notion that JV partners should be included but codeshare passengers outside of a JV will hardly come close to providing an accurate answer of the industry.

But perhaps that is not the intent.

The author does not want to include codeshare partners because if they did they would have to acknowledge that Korean Airlines is the largest Asian carrier across the Pacific and is also a DL partner. Add in all of the other codeshare partners on each side (which other analyses have accurately done) and Skyteam and Star are neck in neck in terms of size across the Pacific.

If you add in other countries, then Skyteam’s codeshare presen ce in China compares very favorably with the rest of the industry but there are no JVs between the US and China because China does not have Open Skies with the US, a prerequisite for the US to grant JVs.

The real question as to why DL has not signed a JV with KE is very obvious from the data. DL carries far more revenue from the US to Japan than KE does; DL has absolutely no incentive to equally share revenue with KE. As long as DL maintains average fares as high as it does between the US and Asia, driven by its performance in Japan, it has no intention of sharing that revenue with anyone.

In contrast, UA and AA both NEED partners in Japan in order to help compete in the largest TPAC market and yet both AA and UA do not have average fares on their own metal as high as what DL has between the US and Japan.

The simple truth is that DL is still the largest single carrier between the US And Japan, the largest between the US and Asia; UA plus NH provide slightly more capacity than DL but AA/JL does not.

The simple fact is that DL carries a far higher percentage of revenue between the US and Japan than any other carrier AND the average fares to Japan are as high as what is carried to other countries in Asia, but on much lower costs.

JL and NH are both aggressively growing with JL trying to use the 787s to add point to point service and open up new destinations while NH is adding capacity in SEA, ORD, and NYC via JFK where it may be trying to go head to head w/ DL in SEA and JFK but where it has the high potential to harm UA’s own Asian presence.

Looking beyond Japan, KE is the largest Asian carrier on a TPAC basis and the 3rd largest carrier overall behind UA and DL.

DL’s Asian based operation is really more like an Asian airline’s in Japan and a US-based airline to non-Japanese destinations. DL inherited an enormously profitable franchise which NW developed and protected over 50 years and which still is a larger TPAC operation than every other airline than UA.

But size alone doesn’t begin to tell the real story. Airlines don’t operate to carry passengers; they operate to generate revenue. The author excluded one of the largest parts of the entire TPAC operation, DL’s Japan-Hawaii flying, intentionally or not, but anyone who understands the industry at all recognizes that DL makes enormous amounts of money flying Japanese tourists to Hawaii and other US territory beach destinations, GUM and SPN. If the author wants to exclude the most profitable part of any carrier’s TPAC operation, he most certainly won’t come close to understanding it.

DL’s Asian operation is really more like an Asian airline’s in Japan and a US-based airline to non-Japanese destinations. The economics continue to favor that DL vigorously protect its Japan presence and grow it. Don't be surprised if DL engages in a few strategic moves to further strengthen its Japan network, which their CEO says accounts to 10% of DL's total revenues; I don't think any other US carrier is as connected to one market as DL is to Japan.

UA continues to be stronger to China and HKG on its own metal but it also incurs higher costs to generate that revenue than DL which gets about the same revenue per passenger even on shorter flights. UA's overall TPAC size is larger than DL's. UA is also stronger than DL to the S. Pacific on its own metal.

Further, you can throw in joint venture revenue if you would like, but in all honesty, don’t act like revenue doesn’t count if it doesn’t come from a JV partner. None of us have any real idea how much revenue each carrier gets from JVs or codeshare partners but it is very certain that they both are very real and large numbers.

I'm sorry but AA's presence in Asia is small and that is reflected in its average fares which trail DL and UA; remember that DL started JFK-NRT after the merger and within a very short time, AA dropped their own service. They replaced it with JFK-HND which generates average fares far lower than what AA gets from MIA-S. America, a far shorter flight. AA is still battling it out in LAX-NRT even though they wanted to move their JFK-HND flight there but their average fare is a fraction of what DL gets to either NRT or HND, despite the crappy slot times.

If you want to have an accurate portrayal of the industry, in this case the Pacific, don’t carve it up into little pieces such that you create a box that you think is sufficiently small enough that you can look good in and then throw in qualifiers to allow your situation to look better while others does not.

Truth comes in two forms. What you want to believe and what really exists. You can choose to believe whichever you wish but the danger of believing the former is that the latter will always become apparent.

Always.

and there are enormous consequences to believing something that is not really the truth.

I'll be happy to get to the real truth regardless of the results.

And, yes, this is a long post because it contains real data and analysis. Those who can't absorb or discuss this kind of data should just move along.

Copying and pasting a few poorly written articles doesn't begin to provide any understanding of the subject.

Let’s start w/ the author's assumptions, which form the entire basis of what is wrong w/ the analysis.

“First, I’ve left off the substantial Delta and United operations that go from Tokyo to secondary cities in Asia. That would make Delta way bigger than American, but I don’t think it matters. American can get that benefit through its joint venture partner JAL. (United also gets that through ANA besides its own Tokyo hub.)”

Say what? You want to exclude DL’s ability to offer connections within Asia but you acknowledge that JL and ANA do the same thing for their Asian partners? So you want to just include TPAC flying as if that someone is all of the market. Sorry, but the logic is seriously flawed.

But let’s look at just the US-Japan market since AA plus JL should help provide mass to help compete with DL and UA plus NH.

We can look at two data sources: DOT revenue data which is heavily partitioned between US and foreign carriers; foreign carriers only have to report revenue to the DOT for operations that involve their JV partners. Thus, there are huge portions of the total market that are hidden from view. US carriers, however, report on the exact same basis to the DOT so revenue data for AA, DL, and UA across the Pacific provide the same answers. There is also private industry sourced revenue data from CRS/GDS but it is becoming increasingly unreliable as carriers shift more and more booking activity to their own websites and internal channels, as much as employees and fans of the CRS/GDS data would like to tell you otherwise.

The second data set is schedules data which is not private and pretty self explanatory. While revenue data provides insight into what is actually flown, schedules data is pretty straightforward.

Given the limitations of revenue data noted above, DOT data still unmistakenly shows that DL absolutely dominates the market between the US and Japan among US carriers, carrying 3X more revenue than UA and 11X more revenue than AA. DL carries HALF of all US-Japan revenue in the DOT database. Furthermore, DL’s average fare is 40% higher than UA’s and 75% higher than AA’s. Although JL and NH revenue has to be assumed to not be complete in the database, they do not have average fares as high as DL either.

Now, since the author is trying to figure out how strong carriers are between the US and Asia, the DOT data is also pretty accurate for US carriers. Even if you look at all of the US to all of E. Asia on US carriers on their own metal, DL is within 1% point of UA in terms of market share yet DL carries more revenue on its own metal?

Why?

Because the US-Japan market is still the largest single market between the US and Asia. Almost half of all US-Asia revenue carried by US carriers is to/from Japan. US carriers don’t carry anywhere close to the amount of revenue that is carried between the US and Japan.

But there’s one more piece of really interesting data. Average fares between the US and Japan carried on US carriers are within a fraction of a percent as those to most other destinations in Asia; yet, Japan is a whole lot closer to Asia, which means UA is flying two to three more hours to China and HKG to carry the same revenue that is carried to Japan.

So, revenue data – not just schedules – clearly shows that DL far outperforms AA and UA between the US and Japan both in terms of market share and average fare.

More on alliance partners later.

Second, I’m only looking at flights between the Continental US and Asia nonstop. I’m talking specifically about the Continental US, because both Delta and United have flights between Honolulu and Asia. Those are primarily focused on Asian travelers on holiday so it’s not really relevant to determining how well US carriers serve Asia for their US-based travelers.

So are you really serious about objectively looking at the market or not? It sure doesn’t appear to .

Wanting to exclude Hawaii-Asia flying so that it provides a “balanced look” at the competitive situation is bull.

Last I checked, Hawaii is part of the US.

Also, last time I checked, nearly half of DL’s total flights between the US and E. Asia are to/from Hawaii with a slightly lower percentage of total capacity since DL uses smaller planes on average to Hawaii than between the mainland.

But both schedule and revenue data show that DL carries about half of all revenue between Hawaii and Asia and has higher average fares; DOT data shows that DL's average fares between the Japan and Hawaii are far higher than US to Europe flying even though the distance is about the same.

But the whole basis the author uses to exclude the data is flawed by saying that US-Hawaii traffic is foreign originating. Can he really be serious in thinking that airline companies really care where the revenue comes from? Has it not dawned on him that commercial airplanes generally operate on international flights between two cities in two countries and that the world has a global currency system which allows for earnings in one country to be traded for earnings in another. Does he really think that we should exclude Honda automobiles manufactured in the US from Honda’s global revenues and earnings?

If he does, then he probably should be writing about lemonade stands in Texas where he doesn't have to be concerned about currency issues or foreign earnings.

But you know the real rub in his assumption?

The majority of revenue between the US and Asia originates in Asia, REGARDLESS of whether you include Hawaii or not. So, if he wants to include only revenue that originates in the US, he lops off a good chunk of the market.

But there is an interesting statistic here as well. DL gets a far higher percentage of its revenue, whether you include Hawaii or not, from Asia originating passenger than do AA or UA.

Lastly, I’m including joint venture flights operated by ANA under United and by JAL under American, because since it’s a joint venture, those flights should be considered their own. Sure, there is work to be done before the experience is seamless, but the path is there.

You do realize, sir, that codesharing without a JV is not a charity operation, don’t you? AA doesn’t put passengers on CX metal (since AA doesn’t fly to HKG with its own metal) just because AA and CX are aviation buds. Airlines make money even on codeshares, which his part of why airline labor doesn’t like them. It is not uncommon in the US airline industry for a carrier to keep 15-20% or more of a ticket they sell (not including taxes) even though the passenger does not fly on their airline.

The notion that JVs are the only way that carriers make money working together is completely wrong. AS cannot have a JV with AA or DL because the US does not allow two US domestic carriers to have antitrust immunity and share revenues yet AS makes all kinds of money carrying passengers for AA and DL, and AA and DL make money carrying passengers for AA.

The notion that JV partners should be included but codeshare passengers outside of a JV will hardly come close to providing an accurate answer of the industry.

But perhaps that is not the intent.

The author does not want to include codeshare partners because if they did they would have to acknowledge that Korean Airlines is the largest Asian carrier across the Pacific and is also a DL partner. Add in all of the other codeshare partners on each side (which other analyses have accurately done) and Skyteam and Star are neck in neck in terms of size across the Pacific.

If you add in other countries, then Skyteam’s codeshare presen ce in China compares very favorably with the rest of the industry but there are no JVs between the US and China because China does not have Open Skies with the US, a prerequisite for the US to grant JVs.

The real question as to why DL has not signed a JV with KE is very obvious from the data. DL carries far more revenue from the US to Japan than KE does; DL has absolutely no incentive to equally share revenue with KE. As long as DL maintains average fares as high as it does between the US and Asia, driven by its performance in Japan, it has no intention of sharing that revenue with anyone.

In contrast, UA and AA both NEED partners in Japan in order to help compete in the largest TPAC market and yet both AA and UA do not have average fares on their own metal as high as what DL has between the US and Japan.

The simple truth is that DL is still the largest single carrier between the US And Japan, the largest between the US and Asia; UA plus NH provide slightly more capacity than DL but AA/JL does not.

The simple fact is that DL carries a far higher percentage of revenue between the US and Japan than any other carrier AND the average fares to Japan are as high as what is carried to other countries in Asia, but on much lower costs.

JL and NH are both aggressively growing with JL trying to use the 787s to add point to point service and open up new destinations while NH is adding capacity in SEA, ORD, and NYC via JFK where it may be trying to go head to head w/ DL in SEA and JFK but where it has the high potential to harm UA’s own Asian presence.

Looking beyond Japan, KE is the largest Asian carrier on a TPAC basis and the 3rd largest carrier overall behind UA and DL.

DL’s Asian based operation is really more like an Asian airline’s in Japan and a US-based airline to non-Japanese destinations. DL inherited an enormously profitable franchise which NW developed and protected over 50 years and which still is a larger TPAC operation than every other airline than UA.

But size alone doesn’t begin to tell the real story. Airlines don’t operate to carry passengers; they operate to generate revenue. The author excluded one of the largest parts of the entire TPAC operation, DL’s Japan-Hawaii flying, intentionally or not, but anyone who understands the industry at all recognizes that DL makes enormous amounts of money flying Japanese tourists to Hawaii and other US territory beach destinations, GUM and SPN. If the author wants to exclude the most profitable part of any carrier’s TPAC operation, he most certainly won’t come close to understanding it.

DL’s Asian operation is really more like an Asian airline’s in Japan and a US-based airline to non-Japanese destinations. The economics continue to favor that DL vigorously protect its Japan presence and grow it. Don't be surprised if DL engages in a few strategic moves to further strengthen its Japan network, which their CEO says accounts to 10% of DL's total revenues; I don't think any other US carrier is as connected to one market as DL is to Japan.

UA continues to be stronger to China and HKG on its own metal but it also incurs higher costs to generate that revenue than DL which gets about the same revenue per passenger even on shorter flights. UA's overall TPAC size is larger than DL's. UA is also stronger than DL to the S. Pacific on its own metal.

Further, you can throw in joint venture revenue if you would like, but in all honesty, don’t act like revenue doesn’t count if it doesn’t come from a JV partner. None of us have any real idea how much revenue each carrier gets from JVs or codeshare partners but it is very certain that they both are very real and large numbers.

I'm sorry but AA's presence in Asia is small and that is reflected in its average fares which trail DL and UA; remember that DL started JFK-NRT after the merger and within a very short time, AA dropped their own service. They replaced it with JFK-HND which generates average fares far lower than what AA gets from MIA-S. America, a far shorter flight. AA is still battling it out in LAX-NRT even though they wanted to move their JFK-HND flight there but their average fare is a fraction of what DL gets to either NRT or HND, despite the crappy slot times.

If you want to have an accurate portrayal of the industry, in this case the Pacific, don’t carve it up into little pieces such that you create a box that you think is sufficiently small enough that you can look good in and then throw in qualifiers to allow your situation to look better while others does not.

Truth comes in two forms. What you want to believe and what really exists. You can choose to believe whichever you wish but the danger of believing the former is that the latter will always become apparent.

Always.

and there are enormous consequences to believing something that is not really the truth.

I'll be happy to get to the real truth regardless of the results.

WorldTraveler

Corn Field

- Dec 5, 2003

- 21,709

- 10,721

oh my goodness.

Someone's feelings have been hurt one more time because they were holding on to the hope that maybe the situation with AA in Asia wasn't as bad as everyone said and then WT came along and smashed those dreams.

If you - the board collectively - wants to discuss the real competitive issues of the industry and specific carriers, then I will post the truth.

If you want to talk about integrated non-rev policies and have a pep rally for your unity as a new airline, you go for it - and I won't participate.

You can decide what you want this board to be.

As long as people want to bring up tangible, factually based discussions about carrier performance and strategy, I'm here to play.

Feel free to believe whatever truth you want; AA wouldn't be in BK today if its mgmt. and internet fan club had realized that I was accurate and serious about my criticisms of AA's strategies more than 7 years ago - and the accuracy of what I said then has been completely validated.

Someone's feelings have been hurt one more time because they were holding on to the hope that maybe the situation with AA in Asia wasn't as bad as everyone said and then WT came along and smashed those dreams.

If you - the board collectively - wants to discuss the real competitive issues of the industry and specific carriers, then I will post the truth.

If you want to talk about integrated non-rev policies and have a pep rally for your unity as a new airline, you go for it - and I won't participate.

You can decide what you want this board to be.

As long as people want to bring up tangible, factually based discussions about carrier performance and strategy, I'm here to play.

Feel free to believe whatever truth you want; AA wouldn't be in BK today if its mgmt. and internet fan club had realized that I was accurate and serious about my criticisms of AA's strategies more than 7 years ago - and the accuracy of what I said then has been completely validated.

OP

- Jul 23, 2003

- 15,988

- 9,428

- Thread Starter

- #5

Perhaps you should argue it directly with Brett in his comments section, WT. That's why it is there. You can even remain anonymous.

I suspect you won't, because there's the risk he or others would actually respond to you.

I'd invite him here (we've known each other for about 15 years), but why should he bother? He's already got a successful blog & business travel website built around his name.

I suspect you won't, because there's the risk he or others would actually respond to you.

I'd invite him here (we've known each other for about 15 years), but why should he bother? He's already got a successful blog & business travel website built around his name.

kirkpatrick

Veteran

"You might be surprised to know that with its joint venture partner JAL, American has onlyonetwo fewer flights per day as compared to Delta between the Continental US and Asia."

Note: with its joint venture partner JAL. Other airlines actually fly places.

MK

Kev3188

Veteran

WorldTraveler

Corn Field

- Dec 5, 2003

- 21,709

- 10,721

I have made it very clear that I have left the industry other than to participate in online chat forums.

I have no desire to debate those who professionally write regarding aviation and I don't intend to write on a professional basis regarding aviation. It is a hobby for me; I gain no income by sharing my thoughts.

I don't outsource my analysis of the airline industry to anyone and I don't call any "professional analyst" a friend; if you'd like to share my thoughts w/ whatever his name is, feel free. I don't really care if he knows what I have said or not.

What has frosted you and a whole lot of other people for a whole long time is that I have very accurately spoken to the real financial issues that exist in the airline with a strong perspective on network and financial performance related issues.

You are the one who posted the article as if you thought you had either found some smoking gun or wanted to bait me.

I responded the way I have responded for years - I provided an accurate analysis of the data; you are welcome to respond to my perspective if you would like.

As long as this forum remains an open forum, I will respond to discussions regarding network and financial issues regardless of whose fan club I might offend.

I will also continue to monitor the performance of various carriers, including AA up to and after the merger; those who want to read will know whether the merger actually delivers the benefits it was supposed to deliver and whether any competitors including DL actually were affected by it.

May I suggest to you and Fluff that if you don't want to see my rebuttal, don't post the article; I would likely have never bothered to go look for the articles you or Fluff posted.

Airlines are not charities. None of the airlines mentioned here have relationships because they like each other. They have relationships because it helps their own bottom line.

IN the case of Asia, DL clearly does not have JV partners because it does not believe it needs them and is not willing to share its revenue to/from Japan, the largest single market where it has the leadership position.

Only if DL creates a JV that very disproportionately gives it credit for its position in Japan will it share revenues w/ other Asian carriers.

For other markets such as Europe, AA, DL, and UA all compete on a JV basis.

I have no desire to debate those who professionally write regarding aviation and I don't intend to write on a professional basis regarding aviation. It is a hobby for me; I gain no income by sharing my thoughts.

I don't outsource my analysis of the airline industry to anyone and I don't call any "professional analyst" a friend; if you'd like to share my thoughts w/ whatever his name is, feel free. I don't really care if he knows what I have said or not.

What has frosted you and a whole lot of other people for a whole long time is that I have very accurately spoken to the real financial issues that exist in the airline with a strong perspective on network and financial performance related issues.

You are the one who posted the article as if you thought you had either found some smoking gun or wanted to bait me.

I responded the way I have responded for years - I provided an accurate analysis of the data; you are welcome to respond to my perspective if you would like.

As long as this forum remains an open forum, I will respond to discussions regarding network and financial issues regardless of whose fan club I might offend.

I will also continue to monitor the performance of various carriers, including AA up to and after the merger; those who want to read will know whether the merger actually delivers the benefits it was supposed to deliver and whether any competitors including DL actually were affected by it.

May I suggest to you and Fluff that if you don't want to see my rebuttal, don't post the article; I would likely have never bothered to go look for the articles you or Fluff posted.

and as sexy as JVs are, the revenue is still shared. I picked up a few things in kindergarten and one of them was that if I have something that someone else wants, I can either choose to share it as a donation, or I can gain something in return.Note: with its joint venture partner JAL. Other airlines actually fly places.

MK

Airlines are not charities. None of the airlines mentioned here have relationships because they like each other. They have relationships because it helps their own bottom line.

IN the case of Asia, DL clearly does not have JV partners because it does not believe it needs them and is not willing to share its revenue to/from Japan, the largest single market where it has the leadership position.

Only if DL creates a JV that very disproportionately gives it credit for its position in Japan will it share revenues w/ other Asian carriers.

For other markets such as Europe, AA, DL, and UA all compete on a JV basis.

Super FLUF

Senior

- Jun 10, 2011

- 313

- 206

Mixed feelings on this.

From the customer POV, It looks like we do provide access to markets through code share. Not quite the great network one hopes for, but enough to get the job done.

From an employee POV it gets a big "meh." Code share does nothing for us.

Still optimistic for internal growth under the new combined company. We can't do any worse than the failed "shrink to profitability" disaster the dream team gave us for the past decade.

From the customer POV, It looks like we do provide access to markets through code share. Not quite the great network one hopes for, but enough to get the job done.

From an employee POV it gets a big "meh." Code share does nothing for us.

Still optimistic for internal growth under the new combined company. We can't do any worse than the failed "shrink to profitability" disaster the dream team gave us for the past decade.

WorldTraveler

Corn Field

- Dec 5, 2003

- 21,709

- 10,721

Your feelings, Fluf, aren't so mixed that you didn't hesitate to throw one more negative vote on my post - just like you have done many times along with your bud FA Mikey.

What is it, Fluf, that you find so objectionable to what I write? Does it really bother you to have the truth put out there for everyone to see?

Does it bother you that someone else can speak to the issues but you can't?

Or maybe it bothers you to find out that all the hope that you and Mikey and others have had in your company is not as solid as you thought. Loyalty is fine - but do it with eyes wide open.

Like E, your interest in the topic and your "I got him" quickly diminishes when you find out that you have looked at skewed data and flawed assumptions.

There is a reason why DL reported a $1.6B profit last year while AA posted an equally large loss. And it had everything to do with not looking at the data you want to believe but the data that tells the truth.

Your union just signed a contract - granted w/ a gun at your temples - in which AA pilots will now have the most expansive codesharing allowed by any US carrier.

"meh" seems more than inadequate to express the sentiment that most US airline unions have for codeshares and JVs.

What is it, Fluf, that you find so objectionable to what I write? Does it really bother you to have the truth put out there for everyone to see?

Does it bother you that someone else can speak to the issues but you can't?

Or maybe it bothers you to find out that all the hope that you and Mikey and others have had in your company is not as solid as you thought. Loyalty is fine - but do it with eyes wide open.

Like E, your interest in the topic and your "I got him" quickly diminishes when you find out that you have looked at skewed data and flawed assumptions.

There is a reason why DL reported a $1.6B profit last year while AA posted an equally large loss. And it had everything to do with not looking at the data you want to believe but the data that tells the truth.

Your union just signed a contract - granted w/ a gun at your temples - in which AA pilots will now have the most expansive codesharing allowed by any US carrier.

"meh" seems more than inadequate to express the sentiment that most US airline unions have for codeshares and JVs.

Super FLUF

Senior

- Jun 10, 2011

- 313

- 206

WorldTraveler

Corn Field

- Dec 5, 2003

- 21,709

- 10,721

Who was the one that started a post trying to proclaim that the new AA would kick DL's butt to the curb?

You started the discussion, couldn't contribute to it, and then act miffed when someone else actually brings facts to the table regarding the real dynamics that exist in the industry.

There are no barriers that stop any member of this forum from posting regarding any airline they want. There isn't "my" forum or "your" forum.

Once again, you and E and everyone else can decide what you want this forum to be.

If you want to discuss financial and competitive and market aspects, I will be here and I will post what I know.

If you want to talk about shift swaps, pilot crew line construction, and throw all kinds of hugs to your new fellow union members, go for it. I won't participate.

You started the discussion, couldn't contribute to it, and then act miffed when someone else actually brings facts to the table regarding the real dynamics that exist in the industry.

There are no barriers that stop any member of this forum from posting regarding any airline they want. There isn't "my" forum or "your" forum.

Once again, you and E and everyone else can decide what you want this forum to be.

If you want to discuss financial and competitive and market aspects, I will be here and I will post what I know.

If you want to talk about shift swaps, pilot crew line construction, and throw all kinds of hugs to your new fellow union members, go for it. I won't participate.

Silver Meteor

Member

- Apr 4, 2011

- 19

- 9

WorldTraveler

Corn Field

- Dec 5, 2003

- 21,709

- 10,721

Similar threads

- Replies

- 0

- Views

- 1K

- Replies

- 0

- Views

- 1K